On October 23, 2024, the European Union adopted new regulations on liability for defective products in the form of Directive 2024/2853 (entered into force on November 18, 2024). Ultimately, the new regulations are intended to ensure a higher level of safety for consumers’ health and property and guarantee them appropriate compensation. Furthermore, the preamble to the act anticipates the need to facilitate innovation and research, and recognizes the upcoming challenges related to the growing popularity of digital services. However, this does not mean that the previous EU legal act on this matter (Directive 85/374/EEC of July 25, 1985) will automatically become null and void, as the new regulations stipulate that it will continue to apply to defective products placed on the market or put into service before its repeal date (December 9, 2026). What other changes has the new directive introduced?

The beneficial owner clause is used in the so-called withholding tax. Withholding tax is a flat-rate income tax collected by a tax remitter based in the country where the income was generated. It is collected before the income (e.g. from dividends) is paid to an entity that does not have its registered office in Poland. Sometimes (e.g. under Article 22(4) of the CIT Act) the tax remitter is entitled to an exemption. This is usually the case if the entity to which the payment will be made is based in the EU, the European Economic Area or a country that is a party to a double tax treaty with Poland. In such a case, it is necessary to determine whether the entity to which the payment is to be transferred is the beneficial owner of the payment and, if so, where it is subject to taxation.

During the 38th NATO Summit in The Hague in June 2025, the importance, strength, and durability of the North Atlantic Alliance were confirmed in a short declaration consisting of only five short points, including the unwavering validity of Article 5 of the North Atlantic Treaty (Washington Treaty) of April 4, 1949.

In this article attention will be paid to the valuation of the company’s shares:

When is a stock valued at the day’s price?

When is a stock valued at its mid-year average price?

The topic will be analyzed from an economic perspective. Additionally, these aspects will include situations in which one of the previously mentioned valuations is used and why it works well in those situations.

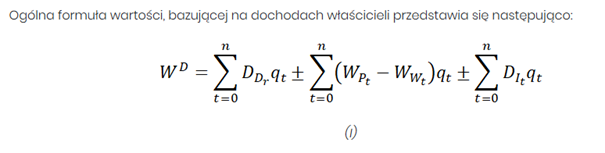

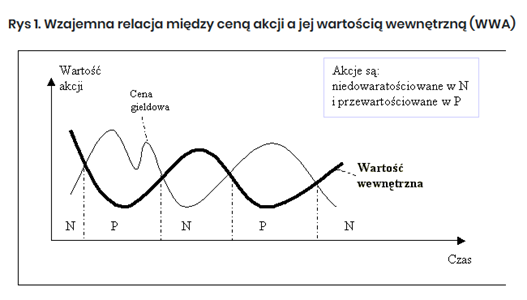

Stock Valuation

Stock valuation is a key process for investors, allowing them to assess investment risk and helping them decide whether to buy or sell a stock. There are several stock valuation methods that provide information about whether a company is undervalued or overvalued.