Due to active involvement in Private Client specialization, the lawyers of KIELTYKA GLADKOWSKI took part in expert contribution about cross border aspects of the rule of law, access to justice system by individuals, publicly funded legal aid for individuals, and alternative civil justice mechanisms in Poland, organized by the key organization World Justice Project within World Justice Project EuroVoices.

The Director of the Institute of Law of the Krakow University of Economics, which is the home of the graduates later on employed by largest state-owned companies in Poland, expressed official gratitude to the lawyers of KIELTYKA GLADKOWSKI for the contribution of our law firm to the continuing education of students of this University and accreditation procedure.

On 31 July 2024 our lawyers took part in a very interesting discussion devoted to selected aspects of M&A in the context of European startups – From scaling to selling: How startup leaders can prep their international workforces for M&A, organized by Sifted.

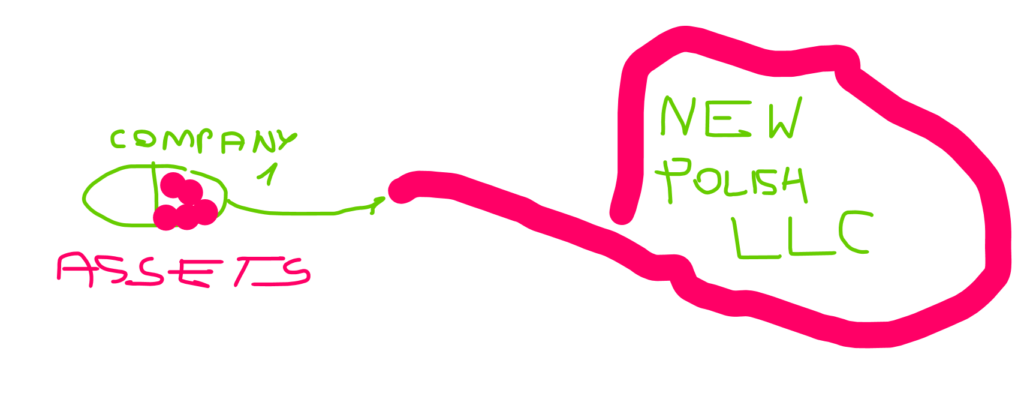

For effective protection of foreign creditors in Polish jurisdiction, our law firm combines the experience of:

1/ the practices of lawyers and litigators who can predict the effects of M&A as a tool for the attempt to remove assets in the face of possible enforcement;

2/ OSINT analysts and private investigators who, using various methods of analyzing metadata, are able to track crypto transactions and information traffic in the Internet, also from the level of DEEP and DARK WEB, and are able to track the real value of the assets of the Polish company.

In recent years, we have seen the dynamic development of the space industry, which is changing our perception of space. One of the most interesting concepts that is gaining popularity as part of this development is Satellite as a Service (SataaS). This model, derived from the broadly understood idea of quality services (XaaS), offers the possibility of using satellite infrastructure and related services based on a subscription model or on demand. This includes both access to satellite data and the use of a variety of satellite functions, such as space observations and satellite communications.

In the context of this dynamic development, legal issues play an important role, which are the foundation of the future of space exploration. International law, European Union regulations and national laws must evolve along with increasing technological capabilities, while ensuring security, sustainable development and fair access to space. We face not only fascinating technological challenges, but also ethical, social and legal dilemmas, the right solution of which can shape our future existence in space.