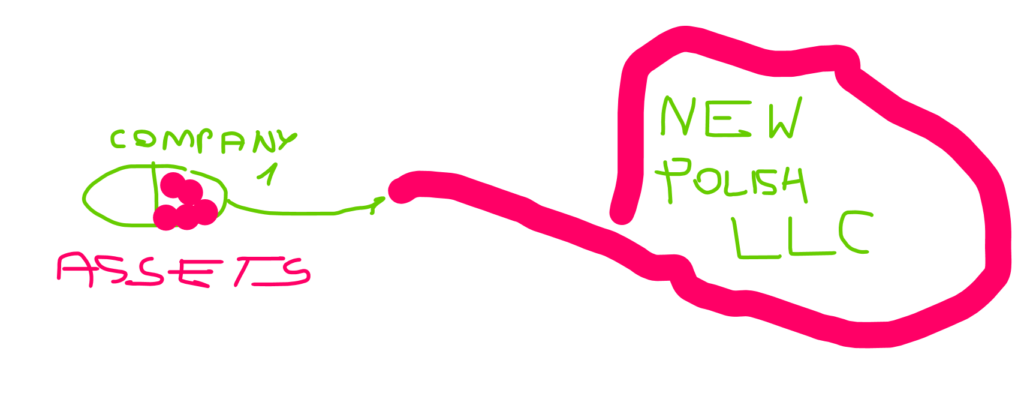

Exit fee is a fee for transferring assets, functions or risks between related entities. It can be understood as remuneration for the transfer of important functions, assets or risks. It is paid during business restructuring, either once or periodicall

On 30 January 2025 there has been issued important interpretation of the Director of the Polish National Revenue Information in respect of exit fee and tax consequences.

The prohibition of discrimination at work is included in Article 183a) of the Labour Code and in the Constitution in Article 32, which requires equal treatment in all aspects, including those related to work.

Discrimination may be related to;

gender,

age,

disability,

race,

religion,

nationality,

views,

origin,

religion or sexual orientation

either due to employment for a fixed or indefinite period or on a full-time or part-time basis.

The above criteria are not socially acceptable and any unjustified unequal treatment of employees is considered discrimination.

Alternative investment companies are a specific form of investment activity introduced into the Polish legal system within the framework of the provisions on investment funds, and specifically in the context of managing alternative investment funds. These regulations are contained in the Act of 27 May 2004 on investment funds and the Act of 22 July 2005 on the management of alternative investment funds, Journal of Laws 2024.1034. AIICs are therefore a specific form of asset management that creates the possibility of investing in alternative assets, such as real estate, private equity, raw materials or debt, while maintaining high flexibility in terms of investment strategies.

For effective protection of foreign creditors in Polish jurisdiction, our law firm combines the experience of:

1/ the practices of lawyers and litigators who can predict the effects of M&A as a tool for the attempt to remove assets in the face of possible enforcement;

2/ OSINT analysts and private investigators who, using various methods of analyzing metadata, are able to track crypto transactions and information traffic in the Internet, also from the level of DEEP and DARK WEB, and are able to track the real value of the assets of the Polish company.

Visiting the American Parliament building by Kiełtyka Gładkowski KG LEGAL’s lawyers. The United States Capitol is a building located on Capitol Hill in Washington, D.C., that serves as the seat of the United States Congress (American Parliament). The visit to the Capitol Hill was related with the role of the members of the American Bar Association as the organization actively engaged in advocacy before Congress, the Executive Branch and other governmental entities on diverse issues of importance to the legal profession.